What the Return of Capital Means for Life Science Manufacturers

For the past three-plus years, many of the most innovative companies in biopharmaceutical and medical technology have been doing something remarkable: advancing life-changing science on a shoestring. Capital was scarce, investors were cautious, and the road to getting a drug or therapy to market felt longer and lonelier than ever.

That’s changing. According to a Wall Street Journal report from January, publicly traded drug and life science companies raised more than $13 billion from new stock issuances in the fourth quarter of 2025 – the highest level in more than four years. Investor confidence in the sector is measurably returning.1

As someone who has spent more than 20 years working alongside biopharmaceutical and medical technology companies, I have a clear view of what this shift means on the ground. It’s genuinely good news, but it’s not a return to the frenzied, throw-money-at-everything environment of 2020 and 2021. This is something better: a rational, discerning market that rewards companies that have done the hard work to get here.

Why the Funding Drought Hit Harder Than Most People Realize

To appreciate what’s happening now, you have to understand what happened between 2021 and 2024. As interest rates rose sharply starting in 2022, investors across the board became more risk-averse, and biopharma, with its long development timelines and high-risk approval process, was an early casualty of that shift. But interest rates were only part of the story. The more consequential dynamic for our industry was a cascading effect through the private capital markets.

During the COVID-19 pandemic, Wall Street’s enthusiasm for biopharma reached extraordinary heights. The mRNA breakthroughs that powered COVID vaccines created a perception of almost unlimited potential for the entire sector. Then, as institutional investors – pension funds, large mutual funds – pulled back from risk assets broadly, it set off a chain reaction. Early-stage venture investors, who might have full confidence in a company’s science and leadership team, began asking a different question: when this company needs its Series B \ raise, will that capital from private equity and institutional investors be there? If the answer was uncertain, they stepped back too.

Many of our customers lived through this reality. They had compelling candidates, strong clinical data readouts, and talented teams, but they were forced to make hard choices. Cut programs. Reduce headcount. Narrow their focus to the one or two pipeline assets they believed could attract secondary funding and see the journey through. The companies that survived this period didn’t just endure; they emerged leaner, more aligned, and operationally sharper than before.

What Separates the Companies That Will Succeed

Now that institutional investors are returning and the second-tranche risk that paralyzed private markets is easing, which companies will be positioned to capitalize? Funders are still being selective, focusing on large addressable markets and clear regulatory pathways. That selectivity hasn’t gone away. It’s no longer accompanied by blanket risk aversion.

From where I sit, the companies built for this moment share a few defining characteristics. Their leadership teams are tightly aligned around a clear strategy. They have disciplined processes for making resource decisions. And critically, they invested, even during the lean years, in the digital infrastructure necessary to grow efficiently that enables efficient execution while maintaining control and compliance during the growth steps now available to them.

That last point matters more than most people outside the manufacturing world realize. When an investor or an auditor walks in, the ability to show digitally enabled processes that maintain control and compliance is proof of organizational maturity and readiness. It signals that this company can execute.

The Critical Question: When Should Infrastructure Planning Start?

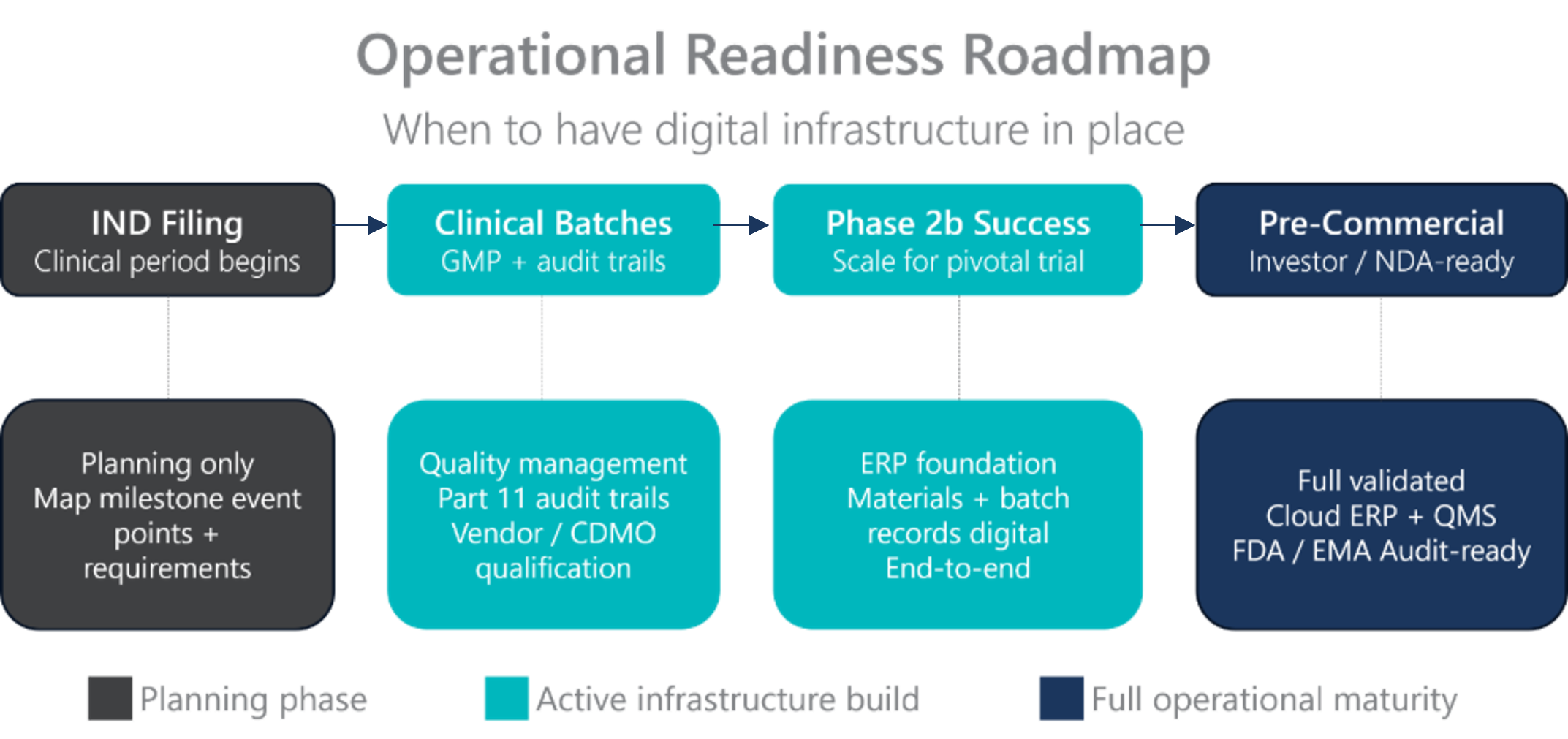

One of the most common mistakes I see growth-stage biopharma and med techs make is treating digital infrastructure as something to tackle “when we get there.” The reality is that operational readiness planning should begin as soon as a company completes its IND and enters the clinical period, not when it’s already racing toward commercialization.

This doesn’t mean going out and licensing a full ERP system and building an IT team on day one. It means mapping the event points along your journey, from first clinical batches and CDMO partnerships, to Phase 2b success and strategic exit conversations, and working backwards to understand what digital capability you need in place leading up to each milestone.

The moment a company begins producing clinical batches, questions of material provenance, vendor qualification, batch approval, and Part 11 audit trails become real. Whether you’re manufacturing internally or relying on a CDMO, the regulatory responsibility rests with you. When the FDA, EMA, or MHRA audits your operation, they want to see that you controlled the process end-to-end and that the data is there to prove it.

The Three Biggest Operational Risks When Biopharma and Medtech Companies Scale Fast

With funding returning and companies preparing to accelerate, the operational risks are very real. In my experience, three stand out.

- Lack of integrated digital infrastructure. When data is entered manually across disconnected systems, the inability to manufacture and document GMP-compliant products can stall a company at exactly the wrong moment. A 483 letter from the FDA, or a failed facility qualification with the MHRA, can have devastating consequences for valuation and timelines. In markets where competitors are pursuing the same therapeutic targets, a stall out can be the difference between winning and losing.

- Inadequate data security and IP protection. Biopharma and Medtech IP is extraordinarily valuable, which makes it an attractive target. No company, not even the largest global life science manufacturer, can replicate the threat detection infrastructure that hyperscale cloud providers like Microsoft operate, with thousands of security professionals working in synch with intelligence tools to monitoring and respond to threats in real time. Being on the right cloud platform is a foundational risk management decision.

- Over-investment in manual processes and headcount. Every dollar spent on people operating manual operational and compliance tasks is a dollar not spent on R&D, clinical trials, or regulatory filings. The right digital infrastructure automates Part 11 audit trails and electronic signatures as a natural byproduct of executing controlled process steps, not as a separate effort requiring a separate team.

One Piece of Advice for Companies with Capital to Deploy

If I could give a single piece of advice to a biopharma or medtech leadership team deploying capital on IT, it would be this: get into a secure, validated cloud environment, and don’t customize the software.

The legacy approach of implementing heavily customized on-premises software, validating a closed environment, and then avoiding upgrades to prevent revalidation is a relic of a different era. Today’s cloud environments offer security, scalability, and automatic access to emerging technologies, including the AI models that are becoming increasingly significant across business functions. EU GMP Annex 22 now provides clear guidance on how deterministic and machine learning models can be used in GMP processes. These capabilities show up natively on leading cloud platforms; if you’re not in the cloud, accessing them requires costly, fragile integration work instead.

Staying with commercially available, off-the-shelf software and avoiding customization also keeps your validation burden manageable. Under the GAMP 5 framework widely used in regulated industries, configured commercial software carries a lower risk classification, meaning you only need to incrementally revalidate the components that changed with each cloud push rather than the entire system.

Starting Smart, Scaling Smoothly

One of the things we’ve worked hard to build at Merit is a pathway for companies to start at the right level of investment for their current stage and expand incrementally as they hit new milestones. Earlier stage companies can begin on Microsoft Dynamics Business Central with Merit’s GMP layer getting compliant, auditable quality and materials management in place without overbuilding. When they reach commercial scale or greater operational complexity, they can migrate to Dynamics 365 with Merit, carrying data and processes forward without starting from zero.

The goal is always the same: spend your raised capital on your science, people, and the clinical work that drives value, not on overbuilt technology infrastructure you don’t yet need. But never find yourself behind, stalling out at a critical event point because the systems aren’t ready. The right platform gets you what you need now, on a foundation designed to grow with you.

An Industry That Refused to Stop Moving Forward

What has been most striking to me through this difficult period is the resilience of this industry. Despite three-plus years of capital constraints, NIH funding uncertainty, and regulatory unpredictability, the companies we work with never stopped innovating. They continued progressing their candidates through clinical pipelines. They made hard decisions and kept moving forward because they are purpose driven and focused on improving patient lives.

Now that the funding environment is improving and institutional investors are returning, many of these companies are in a remarkably strong position. They’ve been battle-tested. Their operations are lean and focused. Some continue to navigate headwinds around NIH funding, but the return of private and public capital should allow them to keep moving forward. The capital returning to them isn’t just enabling growth; it’s accelerating companies that have already earned the right to succeed.

For us at Merit Solutions, we see it in our pipeline, in the conversations we’re having with customers, and in the urgency with which companies are now thinking about getting the right infrastructure in place. We exist to make sure that when the opportunity arrives, our customers are ready to meet it.

Your Science Is Ready. Make Sure Your Operations Are Too.

The best time to map your operational readiness is before you need it.

Merit’s one-day Microsoft Catalyst Envisioning Workshop is designed to help biopharma and medtech leadership teams do exactly that — identify where your digital infrastructure gaps are, prioritize the right investments for your current stage, and build a clear roadmap forward.

It’s one day. The clarity it creates lasts through every milestone that follows.

Frequently Asked Questions: Biopharma Funding and Operational Readiness

Is biopharma funding recovering in 2025 and 2026?

Yes. Publicly traded drug and life science companies raised more than $13 billion from new stock issuances in Q4 2025, the highest level in more than four years, signaling a measurable return of institutional investor confidence in the sector. Unlike the speculative enthusiasm of 2020 and 2021, this recovery is characterized by selective, disciplined capital focused on companies with large addressable markets, clear regulatory pathways, and proven operational maturity.

What caused the biopharma funding drought between 2021 and 2024?

Rising interest rates beginning in 2022 made investors broadly more risk-averse, and biopharma, with its long development timelines and high-risk approval process, was an early casualty. The deeper issue was a cascading effect through private capital markets. As institutional investors pulled back from risk assets, early-stage venture investors began questioning whether Series B and later-stage capital would be available when their portfolio companies needed it, causing them to step back as well.

When should a biopharma or medtech company start planning its digital infrastructure?

Operational readiness planning should begin as soon as a company completes its IND filing and enters the clinical period, not when it is approaching commercialization. Once a company begins producing clinical batches, regulatory requirements around material provenance, vendor qualification, batch approval, and Part 11 audit trails become real obligations. Companies that wait until late-stage development risk stalling at critical milestone events when the cost of delay is highest.

What are the biggest operational risks for biopharma and medtech companies scaling quickly?

Three risks stand out. First, lack of integrated digital infrastructure. Disconnected manual systems can result in FDA 483 observations or failed facility qualifications that derail timelines and damage valuation. Second, inadequate data security and IP protection. Biopharma IP is a high-value target, and no growth-stage company can replicate the threat detection capabilities of a hyperscale cloud provider. Third, over-investment in manual compliance processes. Every dollar spent on manual operational tasks is a dollar not available for R&D, clinical trials, or regulatory filings.

What is a Microsoft Catalyst Envisioning Workshop and how does it help life science companies?

A Microsoft Catalyst Envisioning Workshop is a structured one-day session led by Merit Solutions life science experts that helps biopharma and medtech leadership teams assess their current digital infrastructure, identify gaps relative to their development stage and upcoming milestones, and build a prioritized roadmap for investment. For growth-stage life science companies deploying new capital, it provides a clear and actionable starting point, ensuring technology investments are right-sized for today while building toward the operational maturity required for commercialization and regulatory audit readiness.

Yes. Publicly traded drug and life science companies raised more than $13 billion from new stock issuances in Q4 2025, the highest level in more than four years, signaling a measurable return of institutional investor confidence in the sector. Unlike the speculative enthusiasm of 2020 and 2021, this recovery is characterized by selective, disciplined capital focused on companies with large addressable markets, clear regulatory pathways, and proven operational maturity.

Rising interest rates beginning in 2022 made investors broadly more risk-averse, and biopharma, with its long development timelines and high-risk approval process, was an early casualty. The deeper issue was a cascading effect through private capital markets. As institutional investors pulled back from risk assets, early-stage venture investors began questioning whether Series B and later-stage capital would be available when their portfolio companies needed it, causing them to step back as well. By 2024 many promising companies had been forced to cut programs, reduce headcount, and narrow their focus to the pipeline assets most likely to attract follow-on funding.

Operational readiness planning should begin as soon as a company completes its IND filing and enters the clinical period, not when it is approaching commercialization. Once a company begins producing clinical batches, regulatory requirements around material provenance, vendor qualification, batch approval, and Part 11 audit trails become real obligations. Companies that wait until late-stage development risk stalling at critical milestone events when the cost of delay is highest.

Three risks stand out. First, lack of integrated digital infrastructure. Disconnected manual systems can result in FDA 483 observations or failed facility qualifications that derail timelines and damage valuation. Second, inadequate data security and IP protection. Biopharma IP is a high-value target, and no growth-stage company can replicate the threat detection capabilities of a hyperscale cloud provider. Third, over-investment in manual compliance processes. Every dollar spent on manual operational tasks is a dollar not available for R&D, clinical trials, or regulatory filings.

A Microsoft Catalyst Envisioning Workshop is a structured one-day session that helps biopharma and medtech leadership teams assess their current digital infrastructure, identify gaps relative to their development stage and upcoming milestones, and build a prioritized roadmap for investment. For growth-stage life science companies deploying new capital, it provides a clear and actionable starting point, ensuring technology investments are right-sized for today while building toward the operational maturity required for commercialization and regulatory audit readiness.